Futures Market: Overnight, LME copper opened at $9,435/mt, dipping to a low of $9,431/mt shortly after the opening bell. It then fluctuated upward, reaching a high of $9,563/mt near the close, before pulling back slightly to close at $9,520/mt, up 1.75%. Trading volume reached 20,000 lots, and open interest stood at 289,000 lots. Overnight, the most-traded SHFE copper 2506 contract opened at 77,830 yuan/mt, dipping to a low of 77,770 yuan/mt shortly after the opening bell. It then surged straight up, reaching a high of 78,390 yuan/mt during the session, before consolidating sideways near the close, eventually closing at 78,320 yuan/mt, down 0.84%. Trading volume reached 52,000 lots, and open interest stood at 178,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) At 9 a.m. today, the State Council Information Office will hold a press conference, where the heads of the People's Bank of China, the National Financial Regulatory Administration, and the China Securities Regulatory Commission will introduce the "package of financial policies to support market stability and expectations".

According to CCTV News, Pan Gongsheng, Governor of the People's Bank of China, Li Yunze, Director of the National Financial Regulatory Administration, and Wu Qing, Chairman of the China Securities Regulatory Commission, will attend the conference.

(2) At the invitation of the Swiss government, He Lifeng, Member of the Political Bureau of the CPC Central Committee and Vice Premier of the State Council, will visit Switzerland from May 9 to 12 to hold talks with Swiss leaders and relevant parties. During his visit to Switzerland, as the Chinese head of the China-US Economic and Trade Working Group, Vice Premier He Lifeng will hold talks with the US head, US Treasury Secretary Bessent. From May 12 to 16, Vice Premier He Lifeng will travel to France to co-chair the 10th China-France High-Level Economic and Financial Dialogue with the French side.

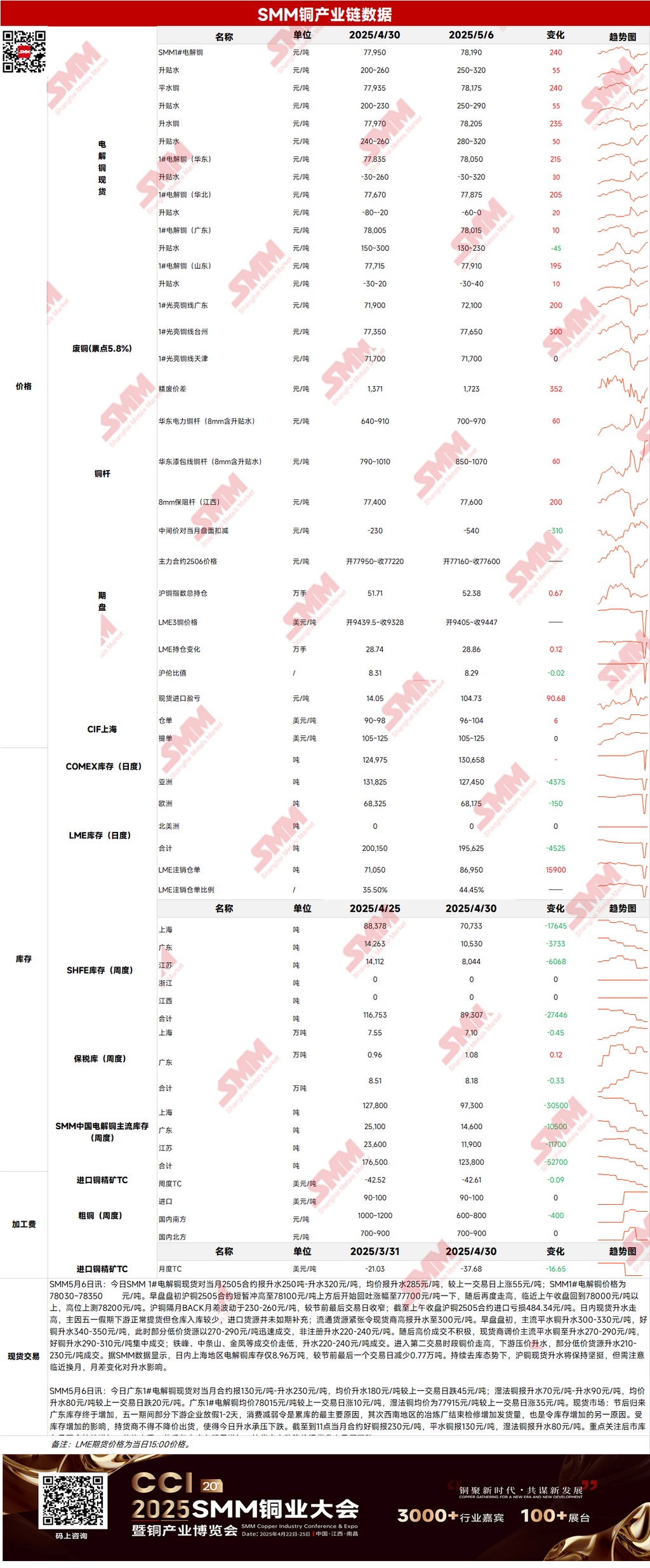

Spot: (1) Shanghai: On May 6, SMM #1 copper cathode spot premiums against the front-month 2505 contract were reported at a range of 250-320 yuan/mt, with an average premium of 285 yuan/mt, up 55 yuan/mt WoW. According to SMM data, Shanghai's copper cathode inventory stood at only 89,600 mt yesterday, a decrease of 7,700 mt from the last trading day before the holiday. Against the backdrop of continuous destocking, Shanghai spot copper premiums will remain firm, but attention should be paid to the impact of price spread changes on premiums as the contract rollover approaches.

(2) Guangdong: On May 6, Guangdong's #1 copper cathode spot premiums against the front-month contract were reported at a range of 130-230 yuan/mt, with an average premium of 180 yuan/mt, down 45 yuan/mt WoW. Overall, inventories increased significantly after the holiday, and suppliers actively lowered prices, causing spot premiums to fall under pressure.

(3) Imported Copper: On May 6, warrant prices ranged from $96 to $104/mt, with a prompt month of May, and the average price increased by $6/mt WoW. B/L prices ranged from $105 to $125/mt, with a prompt month of May, and the average price remained unchanged MoM.EQ copper (CIF B/L) is priced between $65/mt and $75/mt, with QP in May. The average price remained flat on a MoM basis. Quotations are based on cargoes expected to arrive in the first half of May. Overall, both buyers and sellers were active, but trading volume was limited on the first trading day after the holiday.

(4) Secondary copper: On May 6, the price of secondary copper raw materials rose by 200 yuan/mt MoM. The price of bare bright copper in Guangdong was 72,000-72,200 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,723 yuan/mt, an increase of 352 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,375 yuan/mt. According to an SMM survey, after the Labour Day holiday, secondary copper rod enterprises have largely resumed normal production. However, due to the fluctuating trend in copper prices, the circulation of secondary copper raw materials in the market remains limited. Secondary copper rod enterprises anticipate that their production in May will be affected to varying degrees by insufficient raw material supply.

(5) Inventory: On May 6, LME copper cathode inventory decreased by 1,675 mt to 195,625 mt. On the same day, SHFE warrant inventory fell by 3,244 mt to 24,922 mt.

Price: On the macro front, the US Department of Commerce reported on Tuesday that the US trade deficit widened by 14% in March to a record $140.5 billion. Coupled with the decline in the yield of 2-year US Treasury bonds and a series of pessimistic corporate outlooks, this has led the market to refocus on the economic pressure that a potential global trade war could bring. The US dollar index fluctuated downward, which is bullish for copper prices. On the fundamental front, from the supply side, downstream entities normally picked up goods during the Labour Day holiday, but warehouse inflows were limited. Imported cargoes were not replenished as scheduled, leading to tight spot supply. Suppliers' sentiment to hold back cargoes strengthened, pushing spot premiums higher. From the demand side, although some downstream entities made just-in-time procurement in the morning session, overall, downstream purchase willingness was somewhat suppressed by high copper prices, and the market's overall activity was moderate. As of May 6, SMM's copper inventory in major regions across China decreased by 1,100 mt from before the holiday to 128,500 mt on a MoM basis. Looking ahead, if imported cargoes are gradually replenished or downstream demand continues to be suppressed by high copper prices, changes in both supply and demand may alter the current market landscape. Currently, bullish and bearish factors are intertwined in the market, introducing some uncertainty. It is expected that copper prices still have some upside room today.

》Click to view SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and should not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]